Why This Matters to You

If you or someone love receives Social Security benefits. You’ve probably wondered: “Will my check go up next year?” The answer lies in the 2027 Cost-of-Living Adjustment (COLA). Based on the latest forecasts, Social Security recipients could see a social security 2027 cola forecast of about 3.9% in 2027 — a noticeable jump from the 2.8% increase in 2026. That could raise the average monthly benefit by roughly $81, bringing it from $2,081 to $2,162. For many retirees who depend on this income to pay for groceries, medicine, and housing, that extra $972 a year can make a real difference.

Think of COLA like a thermostat for your income. When prices rise (like heating costs in winter), COLA turns up your benefit to keep you comfortable. Without it, rising prices would leave you feeling the chill.

What Is COLA and How Does It Work?

COLA stands for Cost-of-Living Adjustment. It’s the annual increase Social Security adds to benefits to help retirees keep up with rising prices. The adjustment isn’t random — it’s based on a specific measure of inflation called the CPI-W (Consumer Price Index for Urban Wage Earners and Clerical Workers).

Here’s how it works:

- The Social Security Administration looks at the average CPI-W from the third quarter (July, August, September) of the current year.

- They compare it to the average from the third quarter of the previous year.

- The percentage difference becomes the COLA for the next year.

For 2027, that means the final COLA will be announced in October 2026, based on inflation data from July–September 2026. Until then, all forecasts are just estimates that can change as inflation shifts.

The Latest social security 2027 cola forecast – What Experts Are Saying

As of May 2026, the most updated forecast comes from The Senior Citizens League (TSCL), a nonpartisan advocacy group for seniors. They now predict a 3.9% COLA for 2027. This is a big change from their earlier prediction of 2.8% in April.

Why the jump? Inflation has been rising faster than expected. TSCL’s new estimate is based on CPI-W readings that were:

- 2.2% in January and February 2026

- Then spiked to 3.3% in March

The Committee for a Responsible Federal Budget (CRFB), another nonpartisan group, estimates a slightly lower COLA of 3.8%, but agrees the range could be between 3% and 4.5% depending on future inflation.

Independent analyst Mary Johnson even suggests the social security 2027 cola forecast could reach 4.2% if prices for gasoline, energy, and fresh produce continue climbing.

How Much More Money Could Retirees Get in 2027?

Let’s break down the numbers in plain terms:

| Scenario | COLA % | Monthly Increase | New Average Benefit | Annual Extra Money |

| TSCL Forecast | 3.9% | +$81 | $2,162 | +$972 |

| CRFB Forecast | 3.8% | ~$79 | ~$2,160 | ~$948 |

| Early 2026 Estimate | 2.8% | +$57 | $2,081 | +$684 |

For the average retired worker currently receiving $2,081 per month, a 3.9% COLA would add $81.17 to their check, bringing it to $2,162.33. That’s an extra $972 over the whole year.

For those receiving the maximum benefit (around $3,822/month), the increase could be closer to $150 per month or $1,800 annually.

Why Did the Forecast Go Up from 2.8% to 3.9%?

The forecast changed because inflation picked up speed in early 2026. Here’s what drove it:

- Gasoline prices surged in March and April

- Energy costs climbed due to supply concerns

- Fresh produce became more expensive after weather issues

Mary Johnson explained that these three factors — gas, energy, and food — are now pushing the social security 2027 cola forecast higher. Earlier in 2026, when prices were stable, the forecast was 2.8%, matching 2026’s increase. But by May, the tone had changed completely.

It’s like ordering a pizza: if the price of cheese, dough, and delivery goes up, the pizza costs more. Same with COLA — when key prices rise, the adjustment goes up.

What Historical COLA Numbers Tell Us About 2027

Looking at past years helps us understand where 2027 might land:

| Year | COLA % | What Happened |

| 2023 | 8.7% | Highest due to post-pandemic inflation boom |

| 2024 | 3.2% | Inflation cooled but stayed above 3% |

| 2025 | 2.5% | Inflation continued falling |

| 2026 | 2.8% | Slight uptick in prices |

| 2027 (forecast) | 3.9% | Inflation rising agai |

The 2023 jump to 8.7% was a one-time shock. Since then, social security 2027 cola forecast has been trending down until 2026, when it rose slightly. Now in 2027, it’s heading back up — not to 2023 levels, but higher than the last two years.

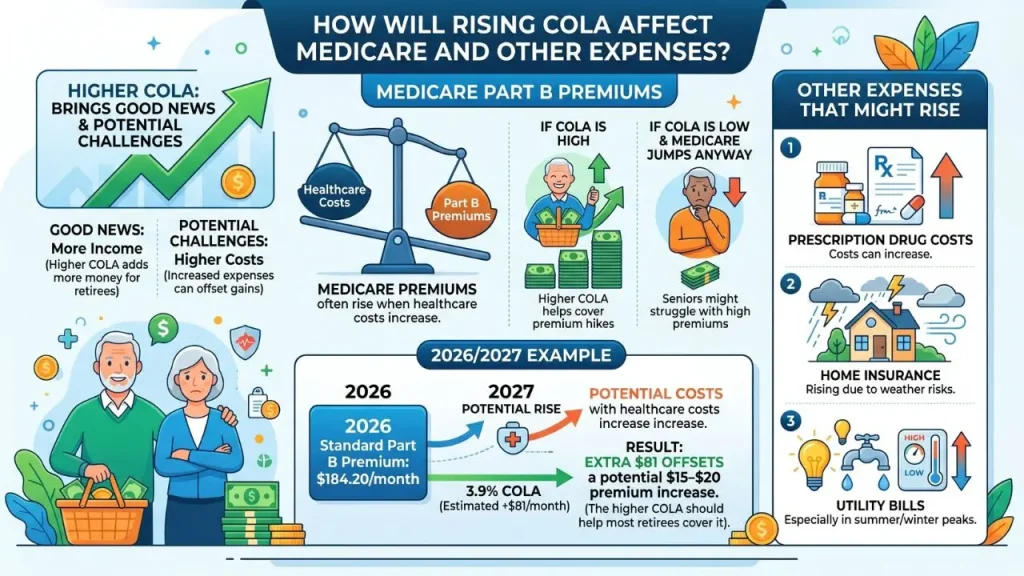

How Will Rising COLA Affect Medicare and Other Expenses?

A higher social security 2027 cola forecast brings good news (more income) and potential challenges (higher costs). The biggest concern is Medicare premiums.

Medicare Part B premiums often rise when healthcare costs increase. If the COLA is higher, more retirees can afford the premium hike. But if social security 2027 cola forecast COLA is low and Medicare jumps anyway, some seniors might struggle.

For 2026, the standard Part B premium was $184.20/month. If healthcare costs rise in 2027, that could go up. However, the 3.9% social security 2027 cola forecast COLA should help most retirees cover it, since the extra $81/month offsets a $15–20 premium increase.

Other expenses that might rise:

- Prescription drug costs

- Home insurance (due to weather risks)

- Utility bills (especially in summer/winter peaks)

When Will the Official 2027 COLA Be Announced?

The official COLA won’t be set until October 2026. That’s when the Social Security Administration releases the final number based on the third-quarter 2026 CPI-W average.

Until October, all numbers are estimates. They can change if:

- Inflation slows down → COLA could drop to 3%

- Inflation speeds up → COLA could reach 4.5%

So while 3.9% is the leading forecast today, treat it as a placeholder until the official announcement.

What If the COLA Is Lower Than Expected?

Some seniors worry: “What if the social security 2027 cola forecast ends up at 2.5% instead of 3.9%?” Here’s what that means:

- A 2.5% COLA would add only about $52/month (vs. $81)

- Annual extra income: $624 (vs. $972)

- That’s $348 less per year

For retirees on a tight budget, that difference could mean:

- Skipping a doctor visit

- Buying cheaper (less healthy) food

- Delaying a needed medication

The good news is that even if COLA is lower, it’s still an increase. Since 2001, COLA has never been 0% — it’s always been positive, even during low-inflation years.

What If the COLA Is Higher Than 3.9%?

On the flip side, if inflation keeps rising, the social security 2027 cola forecast could hit 4.2% or even 4.5%. That would mean:

- 4.2% COLA ≈ $87/month extra → $1,044/year

- 4.5% COLA ≈ $94/month extra → $1,128/year

For someone receiving $3,000/month, a 4.5% COLA adds $135/month or $1,620/year.

This could help retirees:

- Save more for emergencies

- Pay down debt faster

- Enjoy a small vacation or treat

How Can Retirees Prepare for 2027 Regardless of COLA?

Since the final social security 2027 cola forecast isn’t confirmed, it’s smart to plan for different scenarios. Here are practical steps:

- Track your monthly expensesKnow exactly what you spend on food, medicine, and utilities.

- Build a small emergency fundEven $500–$1,000 can help if costs rise unexpectedly.

- Review your Medicare planCheck if you’re on the most cost-effective option for 2027.

- Limit unnecessary spendingCut back on subscriptions or habits you don’t need.

- Talk to a financial advisorMany offer free consultations for seniors.

The 2027 Social Security COLA forecast points to a 3.9% increase, offering retirees meaningful extra income to handle rising costs. While the final number won’t be set until October 2026, knowing the likely range helps you prepare. Whether the COLA ends up at 3%, 4%, or 4.5%, the key is to stay informed, track your expenses, and plan for different scenarios. After all, your benefit is more than a number — it’s your lifeline to comfort and security in retirement.

While retirement planning often focuses on income and benefits, many people also think about how they want to spend their free time. If you’re looking for inspiration, check out our guide to Best Places to Travel Solo Female in US. Which highlights safe and exciting destinations across the country.

Some retirees choose to refresh their homes after leaving the workforce. If you’re organizing a home office, reading corner, or living room, our review of the Nathan James Theo 5-Shelf Ladder Bookcase Variations Colors and Styles 2026 may help you find a practical and stylish storage solution.

Frequently Asked Questions.

1. What is the expected social security 2027 cola forecast for 2027?

The leading forecast from The Senior Citizens League predicts a 3.9% COLA for 2027, which would raise the average monthly benefit by about $81.

2. When will the official 2027 social security 2027 cola forecast be announced?

The official COLA will be announced in October 2026, based on inflation data from July–September 2026.

3. How much more money will retirees get if social security 2027 cola forecast is 3.9%?

With a 3.9% COLA, the average retiree would get an extra $81.17 per month, or $972 over the year, bringing the average benefit to $2,162.

4. What factors could change the social security 2027 cola forecast?

The final COLA depends on inflation trends, especially prices for gasoline, energy, and food. If inflation rises faster, COLA could reach 4.5%; if it slows, it could drop to 3%.

5. Will a higher social security 2027 cola forecast affect my Medicare premiums?

Medicare premiums may rise if healthcare costs increase, but the higher COLA should help most retirees cover the extra cost. The $81/month increase can offset a $15–20 premium hike.

Sources

Social Security COLA for 2027 may be higher as inflation rises, new estimates find

3 Reasons the 2027 COLA Forecast Should Change How You Plan for Social Security Right Now